This article is an on-site version of our Unhedged newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday

Good morning. Instacart’s IPO price, it turns out, was too low. Shares rose 10 per cent yesterday after its debut, leaving the delivery service with an $11bn market cap. Not bad. On a scale from Webvan to Piggly Wiggly, how much is Instacart shaking up the grocery business? Email us your thoughts: robert.armstrong@ft.com and ethan.wu@ft.com.

The US housing market and the substitution effect

Single-family homes are expensive. If you want to own one right now, you have to take out a 7 per cent mortgage on an asset that has risen 40 per cent in price over three years.

So instead of buying a house, you might consider renting an apartment. Rents, at last, have stopped growing like mad. In some metros, they are even falling. Vacancy rates for multifamily units (ie, apartments) have ticked up a bit, suggesting softer demand. And there has been a multifamily building boom, fuelled by a US housing shortage and financed back when rates were low. Construction is the highest on record:

This hasn’t yet shown up fully in building completions, but should soon. Kiran Raichura of Capital Economics projects apartment completions at “historic highs” sometime in the next year, as supply under construction comes to market. This will probably keep rent growth in check.

In principle, the rental and owned-home market are substitutes. A prohibitively expensive single-family home mortgage should push people towards the cooling apartment market, or some other home ownership alternative. But that’s not happening, at least not at scale. Why?

The basic problem is that no part of the rental market is well positioned to offset demand for home ownership, which is still how most Americans want to live. The main rental alternatives fall into three buckets: apartments, build-to-rent (BTR) properties, and renting someone’s existing single-family home.

In apartments, the construction boom has been concentrated in a few high-growth metro areas, especially in the sunbelt, limiting how widely the supply boost may be felt. An oversupply of apartments in, say, Phoenix might some day balance out a shortfall in Los Angeles, but only after years of migration.

Nor are rents particularly cheap. According to Moody’s Analytics, the US rent-to-income ratio in the second quarter stood at 30.2 per cent, just shy of the record-high rent burden reached last year. To the extent it’s playing out, the substitution effect is keeping people who would like to own homes locked into the pricey apartment market, rather than offering homebuyers an affordable alternative, notes Lu Chen of Moody’s.

Importantly, apartments and single-family homes are not direct substitutes. Rick Palacios Jr of John Burns Real Estate Consulting tells us that the majority of BTR tenants they survey who are looking at single-family homes have children and/or pets. That matters, because while 65 per cent of single-family rentals (SFRs) have three or more bedrooms, just 11 per cent of apartments do. For these sorts of buyers, the only realistic options are buying a single-family home, renting one or renting a BTR unit (more on which in a moment). Couples living in a two-bedroom apartment with two dogs and a kid are not, we presume, having a very good time.

So what about SFRs, a closer substitute for traditional home ownership? This is the natural place to look for priced-out homebuyers, Jack Macdowell, CIO of Palisades Group, told us. You don’t get to build equity, but you do get a detached house and a yard near a nice school district.

The problem with SFRs, says Palacios, is that there aren’t enough of them. Even though renting a single-family home is much cheaper than taking out a mortgage on one, SFRs make up only 10 per cent of all housing units. The mortgage rate lock-in effect applies, too. Because no one wants to get a new mortgage at 7 per cent, they also don’t want to move and start renting out their old home. Constrained supply has led to above-trend rent growth in new SFR leases, but the flipside is that SFRs can’t offset demand for home ownership.

Lastly, build-to-rent. These are newer communities of (largely) single-family units meant for long-term renters, often built near schools and boasting yards and garages. Like SFRs, BTR properties are a closer substitute to home ownership than apartments. Their tenants skew higher income and are paying higher rents for better amenities.

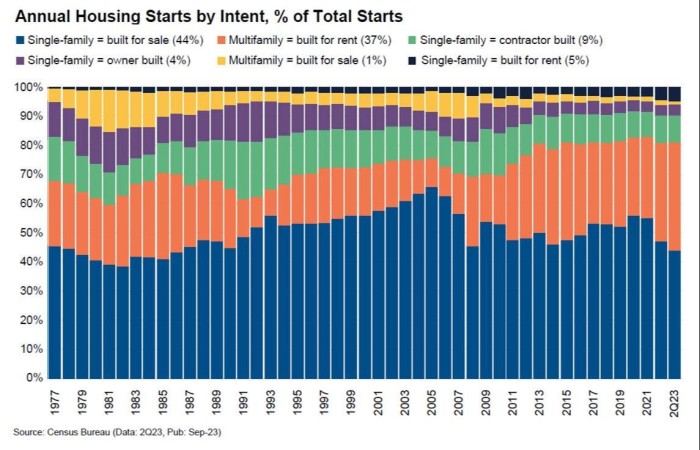

But here, too, Palacios says the problem is scale. BTR housing starts, though they have nearly doubled since the pandemic, are still just 5 per cent of total starts, a rough proxy for market share. Renting an apartment or owning a home remain the biggest games in town. His chart:

The punchline: until rates fall, don’t expect much relief for the housing market. (Ethan Wu)

Oil prices

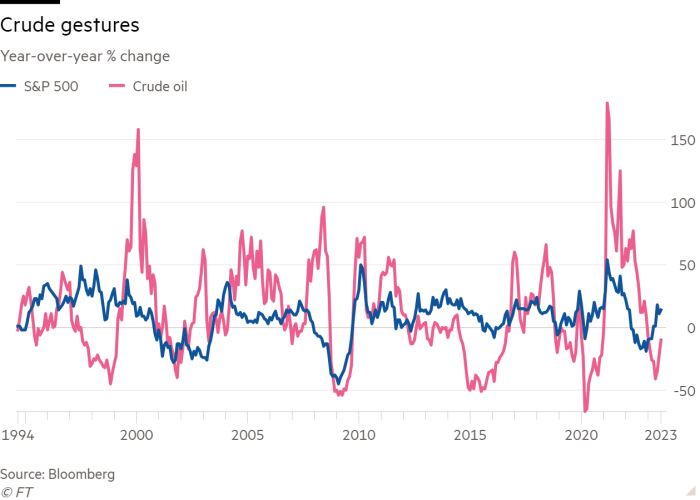

Oil prices passed $95 on Tuesday; they were $20 lower as recently as June. Saudi and Russian supply cuts are having their intended effect. How worried about this should investors be? As my colleague and former boss Stuart Kirk pointed out in his column this weekend, there is no simple relationship between oil prices and bonds, or risk asset prices and oil price shocks, regardless of whether the shock comes from demand or supply. A chart of year-over-year changes in crude prices and the S&P 500 sums up the complexity nicely:

At a glance, there is a strong positive correlation here, but of course that’s because the two prices have a common causal ancestor: recessions and recoveries. If you snip out the synchronised price action around the 2000, 2008 and 2020 recessions, the relationship looks much less determinate. In the late 90s oil prices fell out of bed and stocks flew higher. In the mid-2000s, oil prices jumped, and stocks still managed respectable returns. There is a relationship here, but context matters a lot.

The market context right now has two halves. There are worries about whether inflation will continue to decline, allowing the Fed to cut rates, and questions about whether economic growth can continue its improbably strong run. So we might be concerned about whether higher oil prices will find their way into core inflation indirectly, by pushing up airfares and the like. And we also might be concerned that higher oil prices, by acting as a tax on consumers, will sap consumer spending, which remains the economy’s main growth engine.

These two risks generally cut against each other: to the extent that expensive petrol drives growth down, inflation should be less of a risk. But who is to say that we might not get, say, higher inflation now and lower spending later?

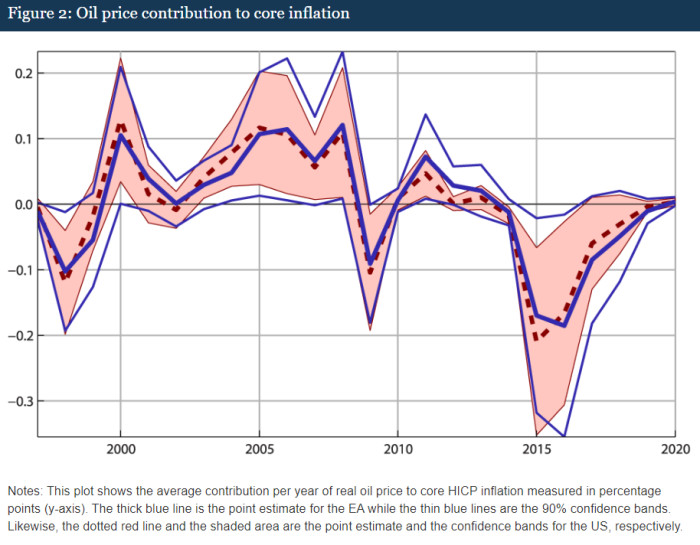

The general consensus among academics and analysts is that the feed-through from oil prices to core inflation is quite limited, unless the rise in prices is particularly large and sustained. A much-cited Fed study published in 2017, in the wake of the 2015 oil price crash, found that the contribution of oil prices to inflation from 1998 through 2019 was never larger than about 0.3 per cent. Its chart:

Ellen Zentner’s economics team at Morgan Stanley concurred last week:

[O]ur previous work finds that a 10 per cent increase in oil prices coming from a negative supply shock adds 35bp to headline CPI for 3 months, but just 3bp to core CPI. Higher energy prices must be sustained for some time to have a greater, more durable effect on core prices. The Fed will look through this shock.

Unless the Russians and the Saudis keep the clamps on for many more months (which they might, for all we know), Unhedged is going to keep the oil/inflation worries on hold.

The worry about growth is a similar story, inasmuch as prices probably haven’t risen enough, for long enough, to hurt spending very much on its own. But the timing is bad, given that we have also had a large, rapid increase in interest rates, and pandemic stimulus programmes are receding farther and farther into the rear-view mirror.

The authors of Deutsche Bank’s long-term asset return study, which we talked about yesterday, finds that about half of the 34 US recessions since 1857 were preceded by a 25 per cent oil price jump in the preceding year. When you combine that with an inflation surge, higher rates and an inverted yield curve, the recession “hit rate” rises to 76 per cent. “All these four triggers have been met for the US. Clearly this doesn’t guarantee recessions but it shows that if a US recession did take place soon, the macro ingredients are in place,” the authors write. A higher oil price makes today’s US economic growth, which is already improbably high, just a bit more improbable.

One good read

Don’t count China out quite yet.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, hosted by Ethan Wu and Katie Martin, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.