Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is head of European equity strategy and head of global derivatives strategy at UBS

Covid really upset the apple cart when it comes to consumption. Most of us experienced the need to upgrade home office technology and equipment and for the lucky ones, buying a pop-up pool in the back garden or a new car.

As Covid restrictions were eased, the Russia-Ukraine war began and kicked off a period of rising energy prices and inflation. Higher interest rates then dealt a big blow in Europe to real incomes, which contracted in 2022 after taking into account inflation. Consumer confidence fell sharply and savings rates rose.

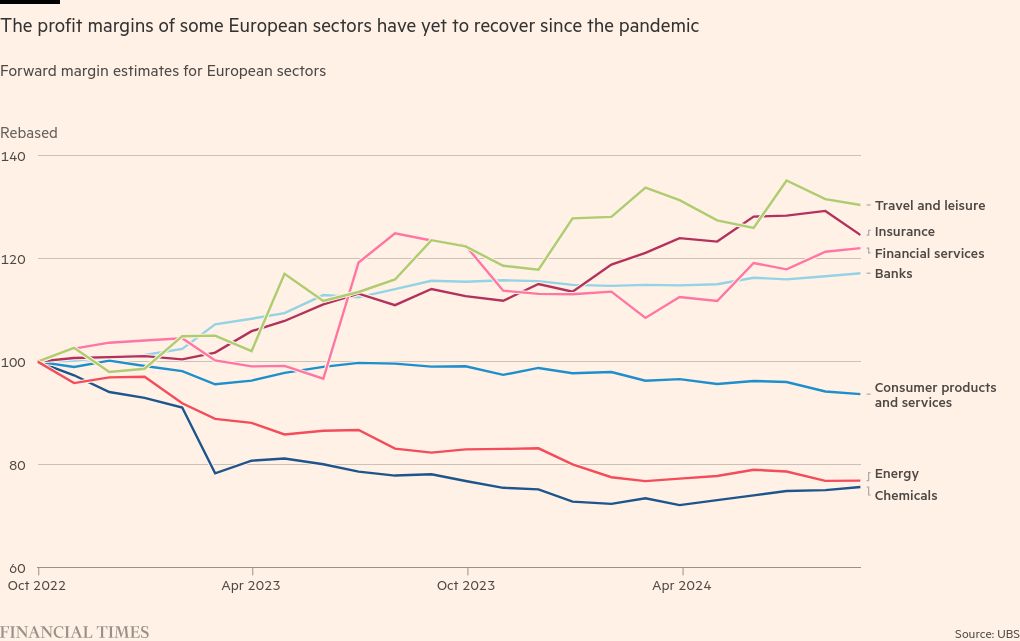

Subsequent spending by consumers was either non-discretionary staple items or “revenge tourism” that supported the recovery for hotels and airlines. Corporate profit margin trends reflected this shift. Margins expanded for financial services, banks, insurance and travel/leisure companies. Margins have been contracting for industrial and consumer goods companies.

Finally, there are now tailwinds for a consumer recovery. Falling inflation and lagged wage growth mean real wages are rising — particularly in the UK. European households have a stock of savings that could be as high as 8.2 per cent of GDP in late 2023. Confidence has been recovering and in some countries like the UK, households have benefited from up to 4 per cent income tax cuts over the past year.

It has therefore been a surprise to many that European consumer companies have been disappointing on profit expectations in the most recent earnings season. Stock analysts highlight that the high-end consumer has been fairly resilient. The weakness in spending appears to be concentrated in the lower-end consumer markets.

The tailwinds are real though. Consumers are showing more willingness to spend. It’s just that progress has been slow. Sreedhar Mahamkali, UBS retail analyst, highlights there is evidence of improvement in UK supermarkets where consumers are consuming more and are buying higher quality products. Aside from this modest transition in demand for consumer staples, there has been little evidence of an improvement in more discretionary spending on goods, clothing, autos or household durables. What gives? Why is the healthy consumer backdrop not translating into a faster recovery in spending?

We think the answer is interest rates. Despite the first rate cuts being delivered by the European Central Bank and the Bank of England, interest rates remain high. The anticipated two-year real rate of interest (after inflation) went from negative 4 per cent in 2022 to positive 1.5 per cent in 2023 and remains at 0.75 per cent recently. This helps explain why the Stoxx 600 Consumer Goods and Services Index has underperformed the Stoxx 600 Index by 30 per cent in the past 18 months and as much as 20 per cent recently year to date.

Low-income consumers are likely to be much more sensitive to interest rates given their exposures to consumer loans, auto loans and leasing and mortgages. However, cheap auto loans set in 2021-22 will progressively come up for renewal. Households lucky enough to fix their mortgage at a low rate during the pandemic, progressively need to remortgage. A single rate cut does little to alleviate these major drags on disposable income.

More rate cuts will ease pressures further and lead to a further transition in consumption habits towards goods and progressively higher value goods, which are usually purchased using loans.

Weakness in China and potentially the US may limit the improvement for some consumer goods companies such as mass-market autos and luxury stocks. However, smaller companies in the economies that are most sensitive to the interest rates and macro tailwinds could benefit more. This includes Spain and Scandinavia but especially the UK. British consumer stocks are up about 13 per cent since the UK election in July.

Hopefully, lower interest rates also will see more housing activity — both transactions and construction. Both would support durables goods companies. Recent announcements by the UK government to increase housing starts could be an important contributor to renewed growth in the UK economy.

In the longer term, more consumer spending on goods should be an important part of the post-Covid story. Money spent on services typically has low “gross value add” — the money doesn’t travel very far. Money spend on goods has higher gross value add as it supports supply chains. The longer and more complex the supply chain, the broader the economic benefits from the spending. Given the likely improving trend on spending on goods in many European economies, investors should take note.