Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Cash is ultimately what every investor would like back from the businesses they own. Complicated structures, indifferent returns and strategic mishaps meant shareholders in composite insurers lost out in recent years. France’s Axa, after suffering from all three, is starting to change that.

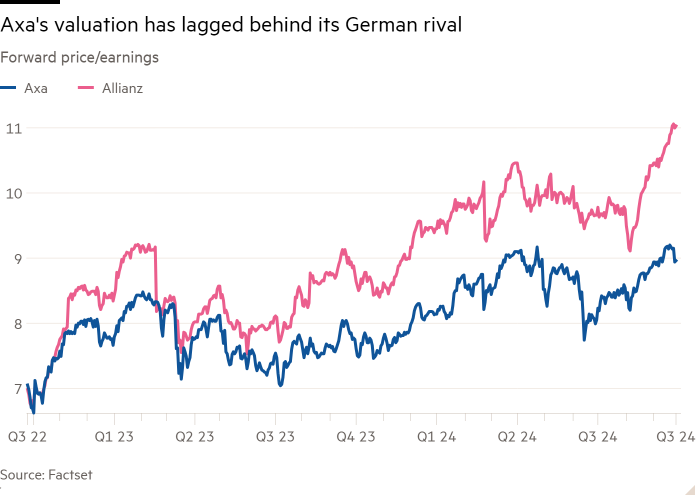

Since Thomas Buberl took over as Axa chief executive in 2016 he has wholly restructured the group and insisted Axa prioritise shareholder returns over acquisitions. That strategy has sparked a rally in the share price, approaching three times its October 2020 low. Yet Axa’s valuation still trails rival Allianz. On a forward price-earnings basis, Axa has yet to cross the 10 times threshold, a level it has rarely traded above since the financial crisis.

Buberl has simplified the group by moving it away from the more capital-intensive life business and into more cash-generative lines such as property and casualty. He has promised Axa will return 75 per cent of its profits, breaking that down into 60 per cent for dividends and 15 per cent to buybacks.

That was a pledge designed to win back shareholder trust, damaged by the poorly executed acquisition of commercial P&C group XL in 2018. Axa overpaid and then spent years getting the business into shape. That appears complete with XL generating €1.9bn of earnings last year. Life now accounts for just a third of Axa group business, down from two-thirds back in 2016. Moody’s last week raised the outlook on Axa’s debt to positive, thanks to reduced earnings exposure to life underwriting risk and a stronger balance sheet.

Composite insurers in general, aware that sector investors distrust anything that isn’t cold hard cash, have shifted away from life policies offering guarantees towards less capital-intensive ones without. Sector remittances — the cash that insurance operations kick up to holding companies — have risen to 80 per cent of net profits from about 60 per cent in 2016, supporting higher shareholder returns.

Axa’s €5.3bn sale of Axa Investment Managers to BNP Paribas, due to be approved next year, could sweeten the deal. Sold at 15 times earnings, Axa plans a €3.8bn buyback to offset earnings dilution. About €1.3bn left, after tax, could be used for bolt-on deals, notes Berenberg — something wary investors will watch carefully.

Over the past three years, Axa has delivered a shareholder return including dividends of more than 85 per cent, half more than the Stoxx 600 insurance index. But it is still relatively lowly rated at 9 times 2025 earnings, compared with Allianz on 11.

Investors still clearly want to see how sustainable this flow of cash into their pocketbooks really is. Expect an affirmative answer in the year ahead.