UK house prices set to slide 10%, Moody’s warns

Rating agency Moody’s has added to the dilemma facing UK housebuyers, by predicting prices will fall 10% over the next two years.

Moody’s believes that persistently high inflation and the recent spike in lending rates will trigger a correction in the UK housing market.

In a report issued last night, Moody’s say:

The combination of less affordable mortgages and high inflation putting a dent in incomes will trigger a correction in the UK housing market.

The relatively large share of short-dated or variable-rate mortgages exposes the existing stock to tightening monetary policy. Strong fundamentals such as a robust labour market, tight underwriting standards and housing supply shortages will prevent more severe credit implications.

Moody’s warns that the correction in UK house prices will be more pronounced than in many other advanced economies.

That’s because the UK has a high proportion of variable or short-term fixed mortgages, compared to other countries such as Germany, the US or France where mortgages have longer maturities.

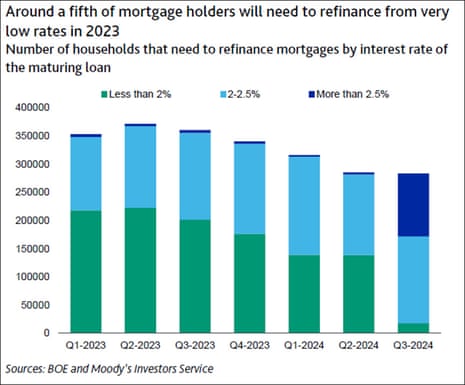

Buy-to-let landlords, who hold 8% of the UK private housing stock, will also influence house prices if a large number choose to sell.

Moody’s say:

To be eligible to refinance, landlords must comply with regulatory requirements to ensure rental income is sufficient to support mortgage payment costs. Landlords can pass on these costs to tenants, but for an average mortgage, this would mean raising rents by close to 20%, according to BOE estimates. Rents are currently increasing by around 5%.

There is anecdotal evidence that landlords are choosing to sell properties instead, putting additional downward pressure on house prices.

Key events

The Bank of England has already raised UK interest rates 12 times since December 2021, as it fights inflation.

Capital Economics warn, though, that the impact of those hikes has not been fully felt yet:

Higher interest rates haven’t dented the real economy much because household incomes have been unusually strong and the interest rates households are actually paying on their loans has not yet risen much.

But there’s an element of keeping the faith here. Higher interest rates will eventually bite harder. Indeed, lots of lenders withdrew their mortgage deals this week and will soon replace them with ones carrying higher interest rates. That’s why we remain in the recession club, even if it’s a lonely place to be.

Sky: George Osborne advisory firm lands role on contested $75bn Call of Duty deal

The UK competition watchdog’s decision to block Microsoft’s takeover of Activision Blizzard annoyed both parties, but the gaming deal could prove lucrative to George Osborne’s City advisory firm.

Sky News are reporting that Robey Warshaw, where former chancellor Osborne is a partner, has landed a key role on the $69bn takeover deal.

They say:

City sources said the firm, which Mr Osborne joined as a partner in 2021, had been involved in the takeover for some time, although its role has not been publicly disclosed.

The deal has become engulfed in controversy after the Competition and Markets Authority’s (CMA) decision to block it.

Regulators elsewhere have approved it, with Microsoft pledging a string of licensing concessions involving rival gaming platforms, prompting the technology behemoth to accuse the UK of stymying innovation.

Earlier this week, the president of Microsoft met with chancellor Jeremy Hunt, amid efforts to overturn the competition watchdog’s decision to block its planned takeover of Activision Blizzard, which makes Call of Duty, World of Warcraft, Hearthstone, and Candy Crush.

Activision has been given permission to intervene in Microsoft’s legal battle with Britain’s anti-trust regulator over its decision to block the deal, Reuters reports today.

Microsoft’s appeal at the Competition Appeal Tribunalis expected to be heard next month, and Activision will also be able to make their case to the tribunal.

Austerity-driver Osborne joined Robey Warshaw in April 2021, and shared a £26.5m payout for his first year working there.

Over in Moscow, Russia’s central bank had left its key interest rate unchanged at 7.5%, but warned that inflation risks are rising.

The Bank of Russia said that prices are rising at a faster rate, but the economy is also strengthening more than anticipated.

It says:

Current price growth rates, including the stable indicators of inflation, continue to increase. Inflation expectations of households and businesses’ price expectations remain high.

Economic activity is rising faster than the Bank of Russia’s April forecast assumed, which in large measure reflects a strong rebound in domestic demand. Accelerating fiscal spending, deteriorating terms of foreign trade and the situation in the labour market remain pro-inflationary risk drivers.

The overall balance of inflation risks has tilted even more to the upside.

The Bank of Russia adds that it could increase interest rates at its next meetings to stabilise inflation near 4%.

It estimates that the current rate of price growth is about 4% per year, but recovering consumer demand and the weak rouble (at a two-month low today) could add to inflationary pressures.

The number of home loan products available in the UK was 5,056 on Friday, according to data company Moneyfacts Group Plc, Bloomberg reports, as lender rush to withdraw and reprice deals.

Bloomberg adds:

That’s about 4% lower than at the start of May, but the highest daily amount this month, suggesting some lenders may be putting deals back on the market at higher rates.

The move is the latest blow to Britain’s cash-strapped homeowners, who are already grappling with higher borrowing costs and a possible drop in house prices. Households are being forced to cut down other expenses to cover higher loan repayments, while many prospective buyers are avoiding the mortgage market altogether.

UK banks, led by HSBC, are removing mortgage deals from the market again as they prepare to reprice home loans to account for inflation https://t.co/t3gy3cIdzu

— Bloomberg UK (@BloombergUK) June 9, 2023

France strong-arms big food firms into cutting prices

Rishi Sunak was lambasted as a latter-day Edward Heath last month, after reports that the government wanted supermarkets to voluntarily limit the cost of essential food items.

But in France, the spirit of state intervention is alive and well, with Paris strong-arming large food suppliers to cut their prices.

The biggest food industry companies in France have pledged to cut prices on hundreds of products from next month, Finance Minister Bruno Le Maire said today, threatening financial sanctions if they break the promise.

The government is furious that prices consumers pay in supermarkets have hit record levels in recent months even though the prices industry pays for many raw materials have been declining.

Le Maire has previously threatened to claw back what he described as “undue” profits from food companies with special taxes if they did not pass on falling raw materials prices to consumers already struggling with high energy prices.

Le Maire told BFM TV on Friday:

“As soon as July, prices of certain products will go down,”

“There will be checks and there we will be sanctions for those who don’t abide by the rules,”

Le Maire mentioned pasta, poultry and oil as some of the products on which prices will be cut.

Back in the City, shares in specialist chemicals firm Croda have tumbled by 13% this morning after it issued a profits warning.

Croda’s crop protection division – which makes chemicals for the agriculture sector – has been hit by “rapid customer destocking” this year. It has also been hit by lower sales of its lipid components which go into Covid-19 vaccines.

The company, based in Snaith, Yorkshire, told shareholders it now expects pre-tax profits of between £370m and £400m this year. Analysts had expected £468m, according to Refinitiv data.

Russ Mould, investment director at AJ Bell, says economic uncertainty is hitting Croda, as well as easing demand for Covid-19 vaccine ingredients.

“The chemicals business soared during the pandemic thanks to its acquisition of Avanti Polar Lipids in July 2020. This made Croda one of the few companies able to make LMPs or lipid nanoparticles, fatty molecules used in drugs and vaccines to encase and protect the stuff in the drugs and vaccines that help people – including in mRNA treatments like the Covid vaccines made by Pfizer and Moderna.

“Inevitably the retreat of the pandemic had an impact on demand in this area and helped to dampen some of investors’ excitement around the business, even if longer-term mRNA has a role to play in other types of medicine.

Ukraine’s gross domestic product fell by 10.5% in the first quarter of the year compared with the same period a year ago, the economy ministry said today.

Reuters has the details:

The ministry said in a statement the fall was less than it had initially expected, indicating the economy was adapting to events following Russia’s invasion more quickly than expected.

The ministry said it had initially expected GDP to fall by 14.1% in the first quarter of 2023.

Over in Italy, factory output has taken a knock.

Italian industrial production index decreased by 1.9% month-on-month in April, and was 7.2% lower than a year ago.

That’s a disappointing economic signal, a day after the eurozone slipped into recession after contracting slightly over the last six months.

Update: ING say:

This is a poor reading, which suggests that softening demand is, for the time being, outweighing the positive effect on supply of improving supply chains and declining energy prices.

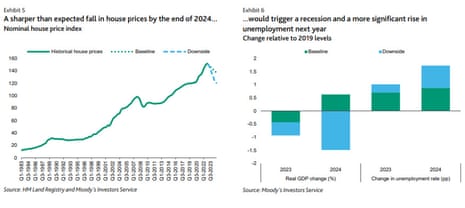

Moody’s have also analysed the consequences of a larger drop in UK house prices over the next two years.

They warn that a hypothetical 21% drop in UK house prices would increase credit risks, and also push the UK into an economic downturn.

In their new report, Moody’s say:

We simulate the macro implications of a 21% decline over two years to assess credit implications for UK issuers.

The UK sovereign would enter a recession in the second half of 2023, lasting for six quarters. Unemployment would reach 6% by end 2024, still below its peak in the global financial crisis.

The UK economy would weaken, but healthy household balance sheets and a highly competitive services sector would soften the blow. Fiscal implications would be more significant, with government debt increasing from already high levels. Banks would face higher credit losses, though a large rise in defaults is still unlikely given the limited increase in unemployment and forward-looking provisions already banks have made.

Buying agent Henry Pryor estimates that house values have already taken a 10% hit so far this year:

If you think you know what your home was worth last Christmas it’s probably worth 10% less today.

We won’t see this in the published data until the deals that are agreed today complete & the prices are published in December. pic.twitter.com/pyBfKHnwcj

— Henry Pryor (@HenryPryor) June 9, 2023

Pryor also reckons it’s ‘business as usual’ in the top-end of the market:

June 2023

🏚 £0-£500k Sticky

🏘 £500-£1.2m Struggling

🏠 £1.2m-£2m Still busy

🏡 £2m-£5m Confused

🏛 £5m+ Business as usual

No science, just a view

— Henry Pryor (@HenryPryor) June 9, 2023

Former Goldman Sachs banker to become Turkey’s first female central bank governor

The glass cliff hypothesis suggests that female executives are more likely to be put in charge when the company is already in a crisis.

And Turkey’s president, Recep Tayyip Erdoğan, is taking the glass cliff theory into monetary policy by appointing the country’s first female central bank chief.

Hafize Gaye Erkan, a finance executive in the United States, has been appointed to head Turkey’s central bank, at a time when high inflation and a record weak currency is piling pressure on policymakers.

Erkan is a former managing director at Goldman Sachs, and is currently a board director at Marsh McLennan. She had been co-chief executive of San Francisco-based First Republic Bank until leaving at the end of 2021 – less than 18 months before the bank was rescued in this year’s panic.

Hafize Gaye Erkan ist neue Präsidentin der türkischen Zentralbank 🏦.

-> Eh. Leiterin Group Analytics für Finanzinstitute @GoldmanSachs.

-> Gründerin First Republic Fellowship, zur Förderung von jungen Frauen in Führungspositionen & eh. Präsidentin @firstrepublic Bank.

— Invest in Türkiye (DACH) (@InvestTR_DACH) June 9, 2023

Although the central bank’s first female governor, Erkan is also its fifth chief in just four years. Erdoğan has sacked several predecessors over policy differences, as he demanded interest rate cuts which have weakened the lira and driven up inflation.

Erkan will replace Sahap Kavcioglu, who spearheaded Erdogan’s rate-cutting drive that set off a historic currency crash in 2021 and sent inflation to a 24-year peak above 85% last year.

Turkish interest rates have been cut from 19% two years ago to 8.5% at present. Inflation fell last month, to 39.6%…..

The news from Turkey overnight replacing the head of the central bank has not helped the Turkish Lira. It has fallen another 1.5% to 23.50 versus the US Dollar

— Shaun Richards (@notayesmansecon) June 9, 2023

.#Turkey’s currency depreciation continues this morning as more people come to the view that, due essentially to competing claims on increasingly-scarce foreign exchange reserves, the Turkish authorities are less willing and less able to intervene in #markets to counter Lira… pic.twitter.com/kdMDSBQ8vb

— Mohamed A. El-Erian (@elerianm) June 9, 2023

High street sales turn negative for first time in more than two years

The UK’s cost of living crisis has driven down sales on the high streets, which turned negative for the first time in more than two years

Total like-for-like retail sales, combining in-store and online, fell by 1.5% overall compared with last May, according to business advisory firm BDO’s latest High Street Sales Tracker.

Online sales fell by 3.3%, one of the lowest results recorded outside of the pandemic, while in-store sales rose by just 1% across the month.

Given the high inflation rates, these figures suggest significant drops in volumes, explains Sophie Michael, head of retail and wholesale at BDO LLP, who called the results “extremely discouraging”.

Miichael adds:

“With three bank holidays last month and the fact that footfall has increased compared to this time last year, these results highlight the huge pressure on the consumer purse.

“The drop in online sales is also stark, recording the worst online sales results on record with the exception of the months impacted by the Covid-19 pandemic.”

The homewares sector recorded a “very poor” total fall of 9.2% in May – as shoppers shunned expensive items such as furniture and electronics. Fashion sales fell 1.5%.

Tesco reported to CMA over pricing of Clubcard offers

Sarah Butler

The consumer group Which? has reported Tesco to the UK’s competition watchdog over the supermarket’s failure to provide detailed pricing information on its loyalty card offers.

The group said the UK’s largest retailer had not clearly explained the unit price of deals for its Clubcard holders – such as the price per 100g or 100ml – so that shoppers could easily compare value for money between different sized packages, bottles, brands and retailers.

It said the lack of unit pricing could be a “misleading practice” under consumer protection regulations because it could make it difficult for shoppers to determine which was the cheapest product.

In one example, Which? found a 700g bottle of Heinz tomato ketchup in Tesco for which the label showed the standard price to be £3.90, or 55.7p per 100g. A prominent Clubcard label showed the same size bottle on offer at £3.50, but the unit price, which would be 50p per 100g, was not given.

At the same time a 910g bottle of the same ketchup on the shelf below was priced at £3.99, or 43.8p per 100g, for all shoppers, making it the cheapest option per 100g. Which? argued many shoppers would wrongly assume the Clubcard option was the best deal available.

UK house prices set to slide 10%, Moody’s warns

Rating agency Moody’s has added to the dilemma facing UK housebuyers, by predicting prices will fall 10% over the next two years.

Moody’s believes that persistently high inflation and the recent spike in lending rates will trigger a correction in the UK housing market.

In a report issued last night, Moody’s say:

The combination of less affordable mortgages and high inflation putting a dent in incomes will trigger a correction in the UK housing market.

The relatively large share of short-dated or variable-rate mortgages exposes the existing stock to tightening monetary policy. Strong fundamentals such as a robust labour market, tight underwriting standards and housing supply shortages will prevent more severe credit implications.

Moody’s warns that the correction in UK house prices will be more pronounced than in many other advanced economies.

That’s because the UK has a high proportion of variable or short-term fixed mortgages, compared to other countries such as Germany, the US or France where mortgages have longer maturities.

Buy-to-let landlords, who hold 8% of the UK private housing stock, will also influence house prices if a large number choose to sell.

Moody’s say:

To be eligible to refinance, landlords must comply with regulatory requirements to ensure rental income is sufficient to support mortgage payment costs. Landlords can pass on these costs to tenants, but for an average mortgage, this would mean raising rents by close to 20%, according to BOE estimates. Rents are currently increasing by around 5%.

There is anecdotal evidence that landlords are choosing to sell properties instead, putting additional downward pressure on house prices.

El-Erian: Inflation is still too high, causing mortgage turbulence

The turbulence in the UK mortgage market is being driven by high inflation, and expectations that the Bank of England will continue to raise interest rates to fight it.

So explains Mohamed El-Erian, chief economic adviser at Allianz and President of Queens’ College, Cambridge.

He told Radio 4’s Today programme:

People expect that the cost of mortgages will go up. And if you are someone who’s going to get a mortgage, you will accelerate the demand for getting that mortgage. Why pay more tomorrow, when you can pay less today?

And if you’re HSBC, you’ve seen lots of people turn up wanting mortgages and you worry about two things. One is will I make money on those mortgages? And two, can I operationally handle these.

HSBC made the judgement that its sustainability, the ability to do business under these conditions, is threatened so it took a very dramatic move.

And all this comes down to a simple fact. Inflation is still too high. And people expect the Bank of England to increase interest rates more.

UK inflation rose by 8.7% in the year to April, four times over the BoE’s 2% target.

City traders expect interest rates will rise again this month, to 4.75%, and could hit 5.5% by the end of this year.

These expectations are pushing up the yield, or interest, on short-term government bonds, which are used to price fixed-term mortgages.

With the recent leg up, the yield on 2-year US government #bonds is nearing 4.60% — some 80 basis points above the low levels of March, April, and early May but short of the 5.07% that prevailed just before the banking tremors.

This comes ahead of two significant events next… pic.twitter.com/PQQnEwKnsM— Mohamed A. El-Erian (@elerianm) June 8, 2023

Mortgage turbulence: what the brokers say

UK mortgage brokers were startled by the speed at which HSBC pulled its mortgage offers for new customers yesterday.

Paul Neal, mortgages & equity release advisor at Missing Element Mortgage Services, says the move came without warning:

Yet again we find ourselves with another lender dropping out of the market until they release new products. This time with no warning.

How are we supposed to give our clients best value when a lender pulls rates with zero notice? This just highlights the importance of a minimum withdrawal period.

Ashley Thomas, director at Magni Finance, says there was a flood of demand after HSBC announced its move yesterday (which is why HSBC ended up pulling deals even earlier than planned):

Unsurprisingly, everyone has tried logging into the system following the announcement. I have been in a queue for a long time and, once I got past the initial wait, I have had several errors/issues.

It is very unfair on clients and brokers with the short notice being given. We have had the same issues before with HSBC when they gave less than a day’s notice.

Katy Eatenton, mortgage & protection specialist at Lifetime Wealth Management, fears other lenders could follow HSBC’s lead:

HSBC is another lender making changes with little notice, making it nearly impossible for brokers to service clients properly. And then to add insult to injury, they pulled them with immediate effect at 3.50pm.….

I’m praying other lenders don’t follow suit. We need to get an industry minimum notice period sooner rather than later, as the status quo simply doesn’t work for consumers.

Introduction: HSBC pulls new mortgage deals after flood of demand

Good morning and welcome to our rolling coverage of business, the financial markets and the world economy.

The turbulence in Britain’s mortgage market has escalated after HSBC temporarily withdrew all its loans with only a few hours’ notice, last night.

HSBC has removed all its residential and buy-to-let products for new customers, with deals becoming available again on Monday. Products and rates for existing customers were still available, though.

An HSBC spokesperson said:

“To ensure that we can stay within our operational capacity and meet our customer service commitments, we occasionally need to limit the amount of new business we can take each day.

“Our broker products will be available again on Monday, June 12.”

But deals are likely to return at higher rates on Monday.

It is the first time that HSBC, which accounts for almost a quarter of the home loans market, has withdrawn from the mortgage market since the aftermath of September’s disastrous mini-budget under Liz Truss’s government.

HSBC originally set a 5pm deadline for securing new deals yesterday, but after experiencing “significant demand”, at 3.45pm it pulled all the remaining deals immediately, as George Nixon of The Times explains:

A few scenes (and angry brokers) in mortgage land today as HSBC sends out first an email saying it will pull *all* mortgage deals from sale due to “significant demand” at 5pm, then another at 3.45pm saying it’ll now do it immediately. Not back on-sale til Monday.

— George Nixon (@George_Nixon97) June 8, 2023

Nationwide also due to increase fixed-rates by up to 0.25% tomorrow too. (But cut trackers)

It’s likely to put a dent in product availability, which bounced back today from 4,597 to 4,831 deals.

Average two-year rate up again to 5.82% today, average five-year fix up to 5.49%

— George Nixon (@George_Nixon97) June 8, 2023

Nationwide Building Society, the country’s second-largest lender, has already pushed up borrowing costs too – increasing its fixed-rate mortgage deals by up to 0.25 percentage points.

Among Nationwide’s changes, it said two, three and five-year fixed-rate deals for people with a 5% deposit will increase by between 0.01 and 0.20 percentage points, with rates starting from 4.69%.

Both lenders acted following the rapid rise in mortgage rates over the past few weeks.

Those moves are being driven by concerns that the Bank of England will continue to raise interest rates, after UK inflation remained stubbornly high in April.

Hundreds more home loan deals have been pulled by banks and building societies over the last week, while rates on new fixed mortgage deals are continuing to rise.

Also coming up today

Britain’s windfall tax on oil and gas producers is being scaled back, the government has just announced, as it tries to boost investment in the North Sea.

Currently 75%, the levy will be cut to 40% if prices consistently return to normal levels for a sustained period, but still remain in place until 2028.

The Treasury says:

This forms part of the Government’s strategy to support households with energy bills whilst providing certainty to investors to secure the long-term future of domestic energy production

The Energy Profits Levy has raised around £2.8 billion to date, helping the Government pay just under half the typical household energy bill last winter.

City investors are watching whether Vodafone and the owner of Three network, CK Hutchison, will announce a long-anticipated merger today.

The agenda

-

9am BST: Italian industrial production data for April

-

11.30am BST: Bank of Russia sets interest rates

-

1pm BST: Bank of Russia holds press conference