Good morning. Two data points from yesterday. One: FedEx, “bellwether of global economic growth,” forecast better than expected revenue growth and its shares rose 8 per cent after hours. Two: Pool Corp, which installs pools, said that pool construction would fall 15 or 20 per cent this year; its shares sank, dragging other pool companies into the deep end with it. How do these two fit together? Email me: robert.armstrong@ft.com.

Housing II

Market failures are more interesting than market successes. When one group of people needs something, and another group produces it, and the two groups trade it at a price that makes both better off, this is a wonderful thing. But we don’t learn much from watching it happen. It’s when markets cannot deliver that the world’s secrets are revealed.

Yesterday I wrote about the US housing market, which is failing to deliver houses at prices consumers can afford. Housing affordability is at its lowest level since at least 2007 and, by some measures, since the early 1980s. In what amounts to a parody of a prober market, demand for houses is falling, inventories are rising, and prices are going up anyway.

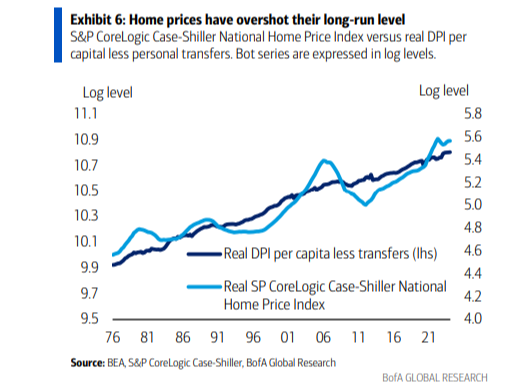

As if to underline my point, the April reading for the industry standard Case-Shiller home price index came out just after yesterday’s letter, and it showed that prices have risen to a new high, breaking a sideways trend. US home prices rose 6.3 per cent from the year before. The index is now 50 per cent above 2019 levels.

Michael Gapen, an economist at Bank of America, argued in a recent report that over the long run the trend in home prices tracks disposable income per capita, and that prices have shot above that trend for the first time since the housing bubble:

How long will Americans have to endure this? The central problem in the existing home market — mortgage lock-in suppressing supply of homes for sale — is well understood, and will simply take time to resolve. A recession and high unemployment would make it happen faster, of course; this is how the affordability problem was solved in 2008. But only an Andrew Mellon-style sadist would root for a recession as a market-clearing device.

In the new-home market, the problem is more of a mystery. As discussed yesterday, housing permits and starts have fallen back to pre-pandemic levels — levels that themselves were inadequate to solve a national housing shortage that dates back at least to the great financial crisis. Why aren’t they building more houses at prices that meet demand?

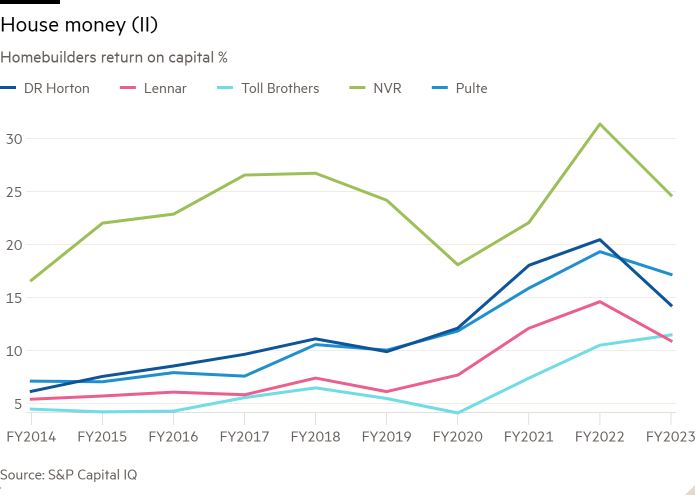

One possible explanation is that cost inflation means that homebuilders are already building as many houses as they can profitably sell. Additional houses, that is to say, could only be built at unacceptable levels of return. But homebuilder margins look pretty good. Gross, operating and net margins for the five largest US home builders are off of their 2023 peaks, but are still very high by the standards of recent history:

The story with return on capital is similar:

Returns at the public companies, strong as they appear, may not be representative of the industry. Rick Palacios of John Burns Consulting emailed that homebuilding is an industry of two halves:

The big publicly traded homebuilders are doing quite well, and the biggest of the big like DR Horton and Lennar are guiding to double-digit growth in 2024. Publicly traded homebuilders as a group are now 48 per cent of all new home sales in the US, up from 22 per cent back in 2003, so a ton of consolidation. The advantages big public homebuilders have over small private builders has probably never been so large

The advantages include a lower cost of capital, scale and in-house mortgage operations. And yet public builders such as Lennar are not targeting higher home deliveries in 2024 than in 2023, just higher revenues.

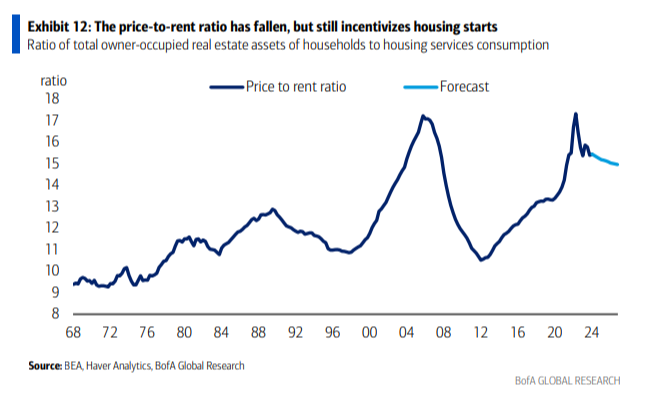

House prices are high enough that they should still be pulling builders and investors off the sidelines. Here is Gapen’s chart of the price-to-rent ratio, which he describes as a return on equity proxy for a new built home:

What the start and permits numbers are telling us, though, is that the industry as a whole is not leaping to capture high returns. Why not? My best guess is that it has a lot to do with the rising inventory of unsold homes, which is approaching half a million units, near the level of the housing bubble years:

In the housing crisis, the homebuilding industry, and investors in homebuilders, learned that excess inventory is a loss waiting to happen. Perhaps the industry is still in shock from 2008 and is therefore over-cautious. In a high-rate environment, carrying inventory can be expensive, as well.

The rise in inventories is, I think, the best single explanation of the fact that the furious rally in homebuilder stocks levelled off a few months ago. The market has, apparently, concluded that the incremental investment opportunities before the industry are not what they were.

But rising inventories are, in a sense, just more evidence of unaffordability. In an undersupplied market, inventory only builds up when it is not priced to meet the buyer. Why don’t the builders sacrifice a bit more margin to do more volume? I’m not sure. Do the public builders, which have the most financial muscle, prize current margins and returns over higher volumes and dollars of profit in the future? Something like this claim is often made about the oil industry in recent years, a result, it is alleged, of the baleful influence of Wall Street short-termism. This would be consistent with the thesis that the industry has been shocked into conservatism by the housing crisis 15 years ago. Alternatively, is the industry too clubby, and not competitive enough? I don’t see evidence of that, but it is possible.

Gapen suggests that one effect of the pandemic was a big shift in housing demand from urban areas to less densely populated areas. This one-time demand shock, he thinks, might explain half or more of post-pandemic home price appreciation. A demand shock like this — not unlike the pandemic supply shocks — simply takes time to be resolved in a new equilibrium. Of course, zoning rules and NIMBYISM have their role to play, too, though the rush to blame them for everything brings out the sceptic in me.

Whether the unaffordability problem has to do with the structure of the homebuilding industry, or pandemic after-effects, or non-market forces, it seems likely to be with us for a long time.

One good read

Fixing Citi is hard work.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.