Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Climate change poses a threat to insurers but it creates opportunities too. Some enthusiasts reckon carbon credits — permits representing the reduction, removal or avoidance of emissions — could be the next billion-dollar insurance market.

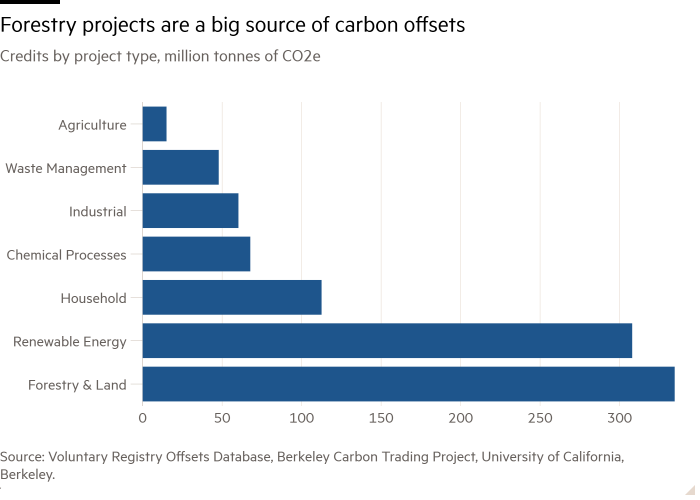

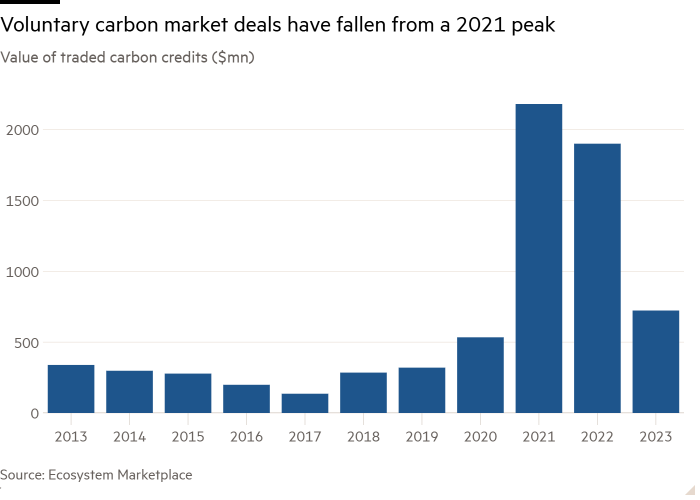

Before that happens, there is a daunting credibility gap to close. Offset projects, which generally set out to “avoid” rather than remove emissions, have often proved to be ineffective or a sham. Forestry projects, which account for nearly two-fifths of all offsets, are threatened by wildfires that have been increasingly frequent and severe. Companies that bought such credits to prove their green credentials have pulled back.

Insurance can address some, but not all, of the market’s problems. It can tackle the risk to buyers who provide advance funding to projects that the credits never materialise. Swiss Re has teamed up with Goodcarbon, a Berlin-based climate start-up, to offer in-kind replacements of insured credits in case of delivery failures of up to five years into the future. UK insurance group Howden has developed a warranty and indemnity policy to underwrite the quality of carbon credits. The policy was recently taken out by Mere Plantations, a UK owner of a Ghana teak plantation, allowing it to charge a premium to the credits’ buyers.

Political risks exemplified by Zimbabwe’s 2023 declaration that all existing offset programmes were “null and void” can also be addressed. The World Bank’s risk insurance arm is set to extend its guarantees to cover risks associated with carbon credits.

The extent to which insurance can tackle “reversal” risk is debatable. Project developers already self-insure against the possibility that carbon captured by a project is re-released into the atmosphere by putting a proportion of their credits into buffer pools. But there are grave concerns about their adequacy. Annual insurance contracts, with premiums that adjust to changing risk, are more credible and transparent than buffer pools, according to Nandini Wilcke, co-founder of CarbonPool, a Zurich-based start-up.

None of this helps much with reputational risk. Companies that snapped up credits and made bold claims have faced accusations of greenwashing. Delta Air Lines is being sued in California over its “carbon neutrality” claims. (It says the case is without legal merit.) FedEx’s annual report recently highlighted the risk that even if regulators accept credits, distrust by third parties could lead to reputational harm.

Clearly, insurance is no silver bullet. But it can play a useful role. For all its problems, the carbon credit market is not about to disappear. Removal projects are vital to limit warming. Offsets will be mandatory for international flights from 2027.

Projects that pass muster with insurers will get added credibility and reduced risk. That could provide a boost to higher quality schemes.